In a world where living costs more, it is difficult to make ends meet when making less money. It is difficult but it is not impossible. Being financially successful (which I am not; still trying) takes some creative strategy on top of the financial intensity strategies I outlined in my previous post. When I was working at a non-profit in North Carolina (The Wilds) I was taking home roughly $980 a month in combined income. Yes, a month! It took a financial situation like that to really help me buckle down and get serious about financial discipline.

How does one live off of $980 a month?! Well, being single sure helped. Apart from that my living situation was actually quite ideal from a financial perspective. My previous post touches on that a little bit. The “debt snowball” was taking a lot of my income because I was very intentional and intense when it came to my debt-free journey. The best advice I can give anyone trying to live off a minimal amount of income is to budget, budget, budget! Making a budget and following the budget are two completely different things that have to coexist in order to work. One can make a budget, but that’s just numbers on paper. One can follow a mental budget, but those numbers can change when there is no reference point for what dollars need to go where. Put the two together and you are not only writing down the numbers, but you are referencing those numbers in order to maintain/track results and keep yourself accountable. The budget works!

Something I learned about budgeting during Financial Peace University was the Zero-Based Budget. You take your projected income and give each and every dollar a place to go until there are zero dollars left to budget. When you tell the money where to go you are no longer wondering where your money went. I remember even just last year I revisited the Zero-Based Budget and found that I had an average of $400 going nowhere and could be applied to debt. That is a significant amount!

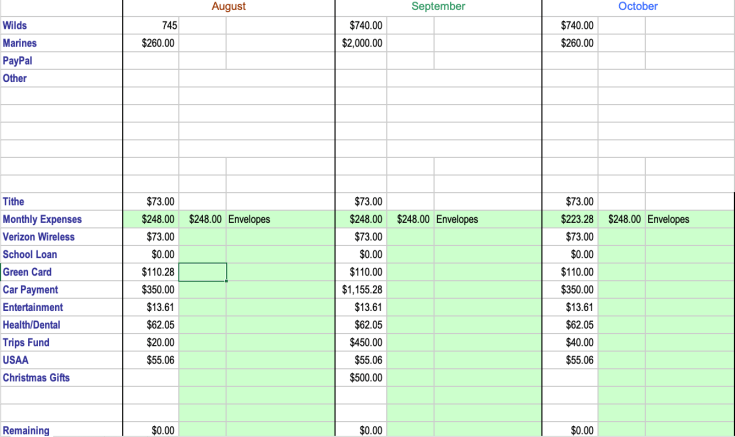

So with a $980 income (The Wilds and Marines combined) my budget was small, but the intensity I had in maintaining that budget and changing my lifestyle showed significant results. Here is an example of how I budgeted that money:

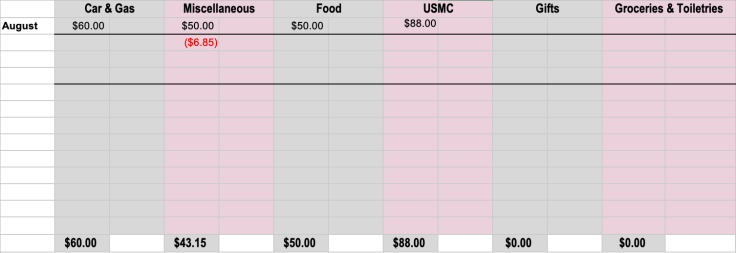

You will notice the income projected is actually about $25 more than $980, but remember that this is just a projection. Should a month produce additional income, put the extra money toward the debt! The main budget has the green highlights and shows income, things that needed to be paid, and a special section for envelopes. The idea of an envelope system is to pull cash out and once the cash is gone, there is no more money to spend. I did that for a while but ended up just tracking my debit card expenses as envelope expenses since it was easier than pulling out cash (everyone operates differently). The grey/salmon columns show general miscellaneous expenses to be paid for with cash. I would track my expenses knowing that once the total reached zero I would no longer have money to spend.

Bear with me for a second as I discuss “envelope rollovers”. Let’s say in August I had $60 set aside for gas/car expenses but I only spent $40. I would roll over $20 to September. When budgeting September, I will only allocate $40 of September’s income to gas/car totaling $60. What do we do with the extra $20? Put it toward the debt! Maybe a birthday is coming up so you put the $20 toward the gift fund. See where I’m going with that? Spending less and having envelope rollovers are the best!

As you can see, the budget I created was very intentional. Each dollar I was making was going somewhere and not in limbo. There was a lot of self-control required in my behavior as well. I often did not eat out and I often declined invitations to paid events. It’s a tough thing to do, but I’ve always defended my lack of spending (especially declining invitations to paid events) by saying,

“I want to spend my money on what I want to spend my money on; not what my friends want me to spend my money on.”

If money is tight, just remember that making a budget and sticking to it will be very beneficial. A tool I have grown accustomed to using is the “EveryDollar” app. This free tool is available on most devices and uses the zero-based budgeting technique I spoke of. Use any tools you find most beneficial for your needs (the example above was in an Excel spreadsheet!). Financial discipline works with a little bit of knowledge and a lot of intentional behavior.

In my next post I plan to share how I was able to pay off $15,000 in the span of 4 months. Remember, I am no expert and I am still on my own financial adventure. In fact, I have been stupid with money for a while. I was, however, truly able to pay off $15,000 in debt in just 4 months. Hope you find this beneficial!

Be strong. Love God. Love others.